Download the PDF

You can download the Competitive Neutrality Policy PDF here or read the full text below.

1. Background to Victoria’s competitive neutrality policy

Victoria is a party to the inter‐governmental Competition Principles Agreement (CPA) which is one of the three agreements that underpin National Competition Policy (NCP). Under the CPA, each state and territory is obliged to introduce and apply competitive neutrality policy and principles to local government and to all government agencies.

The Government is committed to the ongoing implementation of NCP. It notes, however, that NCP does not require:

- asset sales and privatisation

- compulsory competitive tendering

- contracting out

- financial market deregulation

- industrial relations reforms

- reductions in the size of the public sector

- local government amalgamations

- reductions in welfare and social services

- removal of community service obligations (CSOs)1

The competitive neutrality policy framework, as set out in this policy statement, reflects the core intent of NCP.

2. Competitive neutrality policy and principles

The objective of competitive neutrality is set out in Clause 3(1) of the CPA as ‘the elimination of resource allocation distortions arising out of the public ownership of entities engaged in significant business activities: Government business should not enjoy any net competitive advantage simply as a result of their public sector ownership. These principles only apply to the business activities of publicly owned entities, not to the non‐business, non‐profit activities of these entities’.

It is common for private businesses (both for profit and not‐for profit entities) to coexist with government businesses in a variety of markets. They do not always compete on equal terms. Such inequalities arise from a variety of circumstances and it is the goal of competitive neutrality policy to offset these where appropriate. The inequalities of concern arise from differences in tax treatment, differences in the need to provide a return on investment, and related cost advantages or disadvantages which might impact on the prices that are set by government businesses.

The aim of competitive neutrality policy is to account for these factors in such a way that where governments undertake significant business activities in markets, they do so on a fair and equitable basis. Competitive neutrality policy measures are designed to achieve a fair market environment without interfering with the innate differences in size, assets, skills and organisational culture which are inherent in the economy. Differences in workforce skills, equipment and managerial competence, which contribute to differing efficiency across organisations, are not the concern of competitive neutrality policy.

Competitive neutrality can benefit all Victorians by enhancing the confidence of business to make decisions on investments in the State and private decisions as to what to buy and sell.

In general terms, the competitive advantages of public ownership arise from additional costs (or other factors affecting the supply of goods or services) which would be faced by a government business if it were a private firm. For example, a government business which is exempt from paying land tax will enjoy a cost advantage that is not available to a private business operating in the same market. Government agencies should review all of their circumstances and the markets they supply to identify any advantages peculiar to their own circumstances.

Similarly, the competitive disadvantages of public ownership are the additional costs (or other factors affecting the supply of goods or services) which would not be incurred by a government business if it were a private sector business. For example, a government business may have additional accountability and reporting requirements which are not faced by a private business supplying the same goods or services. The key factor in assessing whether a disadvantage constitutes a competitive neutrality issue is that the constraint (on the conduct of the public business) is externally imposed on the agency and it exceeds that

likely to be faced by a private sector business supplying the same goods or services.

See Appendix 1 for further details on the types of differences that will potentially generate cost advantages or disadvantages which may be faced by a public business.

3. The application of competitive neutrality in Victoria

In line with the CPA, competitive neutrality policy applies only to the significant business activities of publicly owned entities, and not to the non‐business non‐profit activities of those entities.

The CPA does not provide a definition of ‘significant business activities’. The Government believes that in making a determination, relevant considerations include the size of the relevant business activity in relation to the size of the relevant market and its influence or competitive impact in the relevant market. An activity should not be regarded as significant or insignificant solely because of its size relative to the overall size of the public or local government business.

In Victoria, it is the responsibility of government agencies and local governments to determine if their business activities fall within the scope of competitive neutrality policy. Agencies and local governments should consult the Victorian Competition and Efficiency Commission (VCEC) if they require assistance in this regard. VCEC is responsible for achieving awareness of and compliance with competitive neutrality policy, including its interpretation and application.

An agency or local government should document its determination as to whether a business activity is, or is not, within the scope of competitive neutrality policy. This documentation should be defensible and will be subject to scrutiny in the event that an investigation is triggered by a complaint.

4. Policy implementation

Competitive neutrality measures are required when the expected benefits of introducing such measures outweigh the costs, and when there are net benefits from implementing such measures having regard to public policy objectives other than competitive neutrality. A range of possible measures may be adopted to achieve competitive neutrality. These include corporatisation, commercialisation and full cost‐reflective pricing.

Corporatisation involves the creation of a separate legal business entity to provide the relevant goods and services. Such an entity is characterised by:

- clear and non‐conflicting objectives

- managerial responsibility, authority and autonomy

- independent and objective performance monitoring

- performance‐based rewards and sanctions

Commercialisation involves organising an activity along commercial lines without creating a separate legal business entity.

This is typically achieved by introducing and applying a set of commercial practices to the business functions of the government agency. The relevant commercial practices, not all of which are needed to achieve competitive neutrality, include:

- clear delineation of commercial and non‐commercial activities, typically through a business plan

- clearly defined commercial performance targets and financial reporting requirements

- separate accounting for, and funding of, non‐commercial activities

- separation of regulatory functions from commercial activities

- an appropriate financial return on the assets used in the commercial activity

- application of a tax equivalent regime

- application of debt guarantee fees

- appropriate financial arrangements for the allocation of profits from the commercial activity

Corporatisation or commercialisation may be unsuitable when the scale of the government business activity is small relative to the non‐commercial or regulatory functions of the agency. This is likely to be the case for local government business activities which are performed as part of a broader local government function (e.g. commercial cleaning by a local government’s cleaning service). In such cases, full cost‐reflective pricing is an appropriate means of achieving competitive neutrality.

Full cost‐reflective pricing takes into account:

- all of the costs that can be attributed to the provision of the good or service

- the cost advantages of public or local government ownership (see Appendix 1 for guidance)

- the cost disadvantages of public or local government ownership (see Appendix 1 for guidance)

The intention of full cost‐reflective pricing is to offset any net competitive advantages a government business may enjoy, thereby ensuring that resource allocation decisions are made on the basis of comprehensive and accurate costing.

In setting the price for the good or service in question, the government agency may have regard to a number of economic factors which include, but are not limited to:

- the level of demand for the good or service

- the level of competition between service providers

- short term pricing strategies involving the use of ‘loss leaders’ or cross subsidisation, subject to the prohibitions of certain pricing behaviour under the Trade Practices Act 1974

For the purpose of competitive neutrality policy, the key requirement of full cost‐reflective pricing is that government agencies and local governments should aim to recover the full costs of their whole of business activity over the medium to long term.

Costing for competitive neutrality and the steps in achieving full cost‐reflective pricing are explained further in A Guide to Implementing Competitive Neutrality.

5. Assessment of costs and benefits

The decision to implement any specific competitive neutrality measure depends, in the first instance, on the expected benefits outweighing the expected costs. The CPA only requires governments to implement competitive neutrality measures ‘to the extent that the benefits to be realised from implementation outweigh the costs’.

Benefits of applying competitive neutrality measures

For the purpose of competitive neutrality policy, an assessment of the potential benefits of applying competitive neutrality measures should include, but is not limited to, the matters outlined below.

- increased market contestability which enables competition in the markets which have been traditionally dominated by public sector businesses. Such contestability produces incentives for businesses to lower prices and provide greater choice for consumers.

- improved performance of government businesses in comparison with competitors. Competitive neutrality increases the incentives for the business to operate efficiently thereby encouraging better use of the community’s scarce resources.

- government‐owned businesses can better clarify non‐commercial objectives, and thereby determine whether the business is effectively meeting these objectives.

In evaluating the beneficial impact of competitive neutrality measures, it is important to remember that the benefits from greater competition will generally arise year after year so that there is a stream of benefits which must be considered. For this reason benefits may be more difficult to establish than costs.

Costs of applying competitive neutrality measures

For the purpose of competitive neutrality policy, an assessment of the potential costs of applying competitive neutrality measures should include, but is not limited to:

- legislative and regulatory amendment

- obtaining information and undertaking analysis to assess appropriate levels for tax equivalents, debt guarantee fees or pricing principles

- administration of tax equivalent and debt guarantee frameworks

These are mainly what might be generically termed ‘transaction costs’ and arise directly from, or are associated with, the process of implementing competitive neutrality measures.

A government agency will need to undertake a public interest test if it considers that another policy objective or objectives of Government would be compromised by the implementation of a competitive neutrality measure. This is discussed further in Section 6.

Weighing up costs and benefits of competitive neutrality measures

Competitive neutrality measures need not be applied when costs exceed benefits, that is, the stream of competitive costs incurred over time is greater than the corresponding stream of benefits accrued over the same period.

In general, the costs of implementing competitive neutrality measures are more immediate, faced by the public business itself and more measurable. The benefits, which tend to accrue over the medium to longer term and diffuse across the community as a whole, are less easily quantified.

It is important that any comparison of costs and benefits is undertaken on the same basis. This can be done by amortising costs over the period for which the benefits are expected to accrue, or converting both the cost and benefit streams to their current values so that they can be compared properly. In this regard, the costs of implementation in most cases are likely to be small relative to overall expenditures relating to the significant business activity.

The cost‐benefit assessment should be documented and made available in the event that an investigation is triggered by a complaint.

6. A public interest test

Balancing competitive neutrality measures with public policy objectives

Once a government agency or a local government has determined that the activity in question is subject to competitive neutrality policy and the expected benefits of introducing the relevant competitive neutrality measure outweigh the costs, it would then need to consider whether implementation of the measure is in the public interest.

Government agencies and local governments are responsible for achieving an array of social, environmental, economic and regional objectives. It is the Government’s intention for competitive neutrality policy to be implemented responsibly and sensitively, recognising these other potential objectives.

The CPA provides some guidance on the matters which should be taken into account in assessing the application of competitive neutrality measures, but it does not address the weighting which governments should apply to such matters. These include:

- government legislation and policies relating to ecologically sustainable development

- social welfare and equity considerations, including community service obligations

- government legislation and policies relating to matters such as occupational health and safety, industrial relations and access and equity

- economic and regional development, including employment and investment growth

- the interests of consumers generally or a class of consumers

- the competitiveness of Australian business

- the efficient allocation of resources

This is an open‐ended list. Other relevant matters can be considered as appropriate. These may include:

- local policies relating to economic and business development, local employment, quality of goods and services, including timeliness of supply

- impact on the local community

- impact on the State and national economies, if any

When a department, agency or local government considers that implementing a competitive neutrality measure would compromise other public policy objectives, it will need to conduct a public interest test to demonstrate the case for not implementing the measure in question. To satisfy the requirements of competitive neutrality policy, the test should, at a minimum:

- clearly identify the policy objective(s) that is to be achieved and ensure that the policy objective(s) has official endorsement (for example, stated by a Minister, a local government body or in an official policy document)

- demonstrate that the achievement of the stated policy objective(s) would be jeopardised if the particular competitive neutrality measure under consideration was implemented

- determine the best available means of achieving the overall policy objectives, including an assessment of alternative approaches

The public interest test should be undertaken in consultation with the community through an open and transparent process. At the conclusion of the process, the conduct and outcomes of the public interest test should be documented and made publicly available. Information that is commercial in confidence may be excluded, provided this is noted in the public documentation.

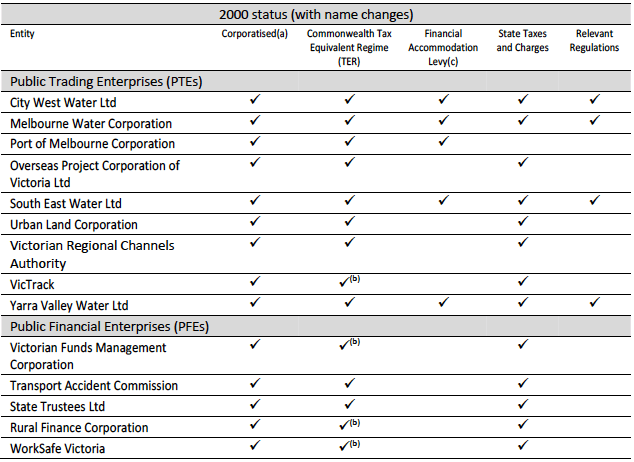

7. Government business enterprises and competitive neutrality policy

The Competition Principles Agreement (CPA) imposes specific competitive neutrality requirements for government business enterprises (GBEs)2. The CPA requires that governments adopt a corporatisation model for GBEs when the benefits of this approach are expected to outweigh the costs. In Victoria this requirement has been met.

For those GBEs where it is determined that corporatisation would not deliver a net benefit to the community, the CPA requires that they are subject to taxation, financial and regulatory requirements equivalent to the private sector. This parity is achieved by subjecting the non‐corporatised GBEs to:

- Commonwealth, state and territory taxes or tax equivalent systems

- debt guarantee fees to offset the advantages of government guarantees

- equivalent regulatory requirements as private sector businesses, for example environment and planning regulations

Further details on the application of this ‘equivalence’ requirement to GBEs in Victoria are provided in Appendix 2.

8. Compliance and the complaints mechanism

Individual departments, agencies and local governments are responsible for:

- identifying the activities to which competitive neutrality policy applies

- taking the necessary actions to comply with competitive neutrality policy

- documenting the decisions they have taken and making the material available to the public on request

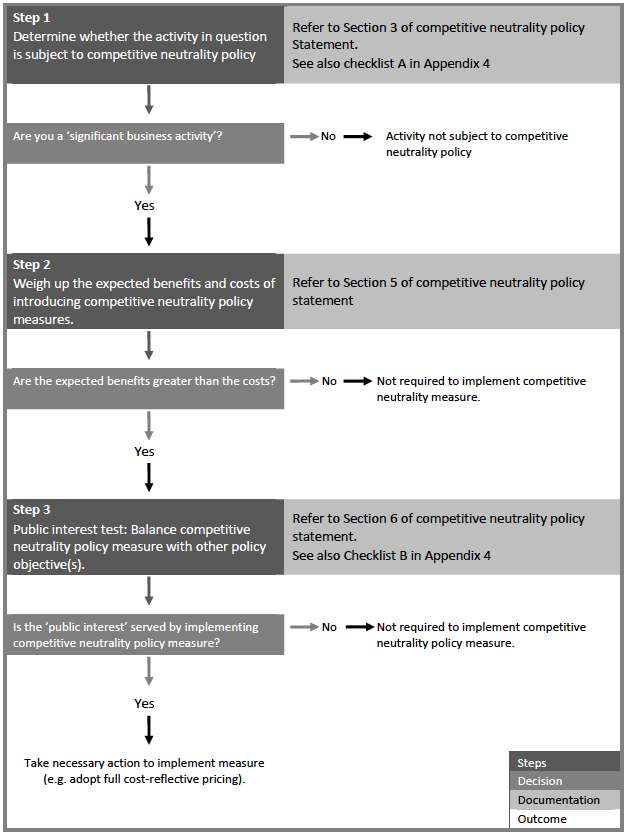

Departments, agencies and local governments should refer to the flow diagram in Appendix 3 and the implementation checklists in Appendix 4 for further guidance.

Compliance by government agencies and local governments

The actions taken by agencies to comply with competitive neutrality policy need to reflect the circumstances of the particular significant business activity and the responsible area of government.

Government departments and agencies, including local governments, are required to be able to demonstrate full observance of the requirements of competitive neutrality policy. Chief Executives (in the case of internal department activities, Department Secretaries) are required to affirm compliance with the Policy for all significant business activities. Acknowledgment is also required in the annual report of the relevant public body.

In the event that a competitive neutrality complaint is received, information demonstrating how the government agency or local government has applied its competitive neutrality obligations will be requested by VCEC.

The complaints mechanism

Under the inter‐governmental CPA, the Government is obliged to introduce and apply the principle of competitive neutrality to all significant business activities in the public sector. This means that all government bodies in Victoria are required to undertake their significant business activities in accordance with competitive neutrality policy. VCEC therefore operates on the assumption of compliance rather than non‐compliance.

If a complaint against a government business’s application of competitive neutrality is lodged, the VCEC determines the extent to which the agency’s actions comply or do not comply with competitive neutrality policy. VCEC provides private businesses with an independent avenue to verify the compliance of a particular government business.

There is a number of important procedural and administrative features of the complaints mechanism. VCEC:

- accepts complaints from a directly affected person or business, as well as from industry or community groups. Complaints are assessed in accordance with competitive neutrality policy. When a complaint is received, the first response of VCEC is to seek verification from the subject agency or local government as to its compliance with competitive neutrality policy

- cannot initiate an investigation

- abides by principles of procedural fairness and investigates accepted complaints fairly, independently and rigorously and comes to a finding on the basis of the best available information. When VCEC recommends a course of action which a government agency or local government should take to comply with competitive neutrality policy, it requests further information to follow up on how compliance with competitive neutrality policy has been achieved

- consults with, and seek comments from, all parties involved before finalising its investigation

- provides finalised investigation reports ‐ excluding any commercial in confidence information ‐ to the parties and publishes them on VCEC’s website

- has no enforcement powers

- does not recommend any compensation or termination of contractual arrangements

VCEC does not assess anti‐competitive behaviour that is already covered by the Competition and Consumer Act 2010 or the Competition Policy Reform (Victoria) Act 1995, nor does it deal with probity issues arising from tendering processes of government agencies or local governments.

The contact details for VCEC on competitive neutrality matters are:

Victorian Competition and Efficiency Commission

GPO Box 4379

Melbourne 3000

Phone: 9092 5828

Email: cn@vcec.vic.gov.au

More information about the way VCEC interprets and applies competitive neutrality policy and carries out its function is available on VCEC website: www.vcec.vic.gov.au

Appendix 1

Some potential cost advantages faced by government departments, agencies and local governments

| Advantages through exemption from: | Description |

|---|---|

| Payroll tax | Levied on firms whose annual payroll is over $515,000. |

| Land tax | Annual tax based on total unimproved value of Victorian land owned by a taxpayer. |

| Stamp duty | Duties are charged on a number of tradeable instruments. |

| WorkSafe Victoria premiums | Levied on employers to cover WorkSafe Victoria expenses. |

| Local rates and charges | Imposed on land. |

| Capital cost | Requirement to earn a rate of return on funds which could otherwise be used elsewhere. |

| Corporate overheads | Requirement to cost various corporate overheads that it has access to, including office accommodation, payroll services, human resource services, marketing and IT services. |

| Capital financing | Requirement to cost an appropriate risk premium where the agency is backed by an explicit or implicit government guarantee. |

Some potential cost disadvantages faced by government departments, agencies and local governments

| Disadvantages due to government ownership | Description |

|---|---|

| Employment remuneration and awards |

The public sector has different employment and industrial relations requirements. For example, a public sector agency may, in comparison to its private sector counterparts, incur a disadvantage due to higher rates of pay under public sector awards. |

| Accountability costs | Greater accountability costs due to public sector reporting and regulatory requirements, where these are greater than the requirements under the Corporations Act 2001 (Cth). |

| Corporate overheads | Limited flexibility in reducing or restructuring corporate overheads. |

| Government agency specific legislation, regulation or directives |

Compliance with various Commonwealth and State legislation, e.g. FOI and restrictions on investment powers. |

Appendix 2

Based on a 2000 assessment the status of the significant government business enterprises is as follows.

a) Clause 3(4) of the CPA states, in part, ‘... for significant Government business enterprises which are classified as ‘Public Trading Enterprises’ and ‘Public Financial Enterprises’ under the Government Financial Statistics Classification: (a) the Parties will, where appropriate, adopt a corporatisation model for these Government business enterprises ....’. This column indicates where a corporatisation model has been implemented.

b) Subject to income tax equivalent payments only.

c) Applicable to all PTEs/PFEs with borrowings in excess of $5 million.

Appendix 3

Appendix 4

Competitive neutrality policy Implementation checklists

|

Checklist A ‐ Determine whether the activity in question is subject to competitive neutrality policy |

|---|

| Identify the context in which the relevant output from the activity (i.e. goods and/or services) is produced and provided to the community. |

| Assess the significance of the size of the business activity relative to the size of the relevant market. |

| Assess the significance of the business activity’s actual and/or potential impact in the relevant market. |

|

Document the determination as to whether the business activity is, or is not, within the scope of the Policy. |

| Checklist B - Public interest test: Balance competitive neutrality policy measures with public policy objectives |

|---|

| Identify the policy objective(s) that is to be achieved and provide supporting documentation, e.g. statement by a Minister or local government body, or official policy documents. |

| Demonstrate that the achievement of the stated policy objective(s) would be jeopardised if the competitive neutrality measure under consideration was adopted. |

| Determine the best available means of achieving the overall policy objectives, including assessing of alternative approaches. |

Document the conduct and outcomes of the ‘public interest test’ and make the documentation available to the public. Information that is commercial in confidence may be excluded, provided this is noted in the public documentation. |

Footnotes

1. Productivity Commission, Impact of Competition Policy Reforms on Rural and Regional Australia, Inquiry Report, 8 September 1999, page 316

2. Government business enterprises include public financial enterprises and public trading enterprises as defined by the Government Financial Statistics Classification.

Updated