June 2024

Notable market developments

- Victoria's Container Deposit Scheme (CDS Vic) has passed its sixth month of operation. Beginning in November 2023, the container returns continue to increase, and Victoria’s network of refund points continue to grow to meet demand, making the scheme the most convenient and accessible in the country.

- Visy’s expanded Laverton glass beneficiation plant is now operating. The new plant can optically sort glass down to 3mm in size (previously it was down to 10mm in size). The resulting cullet will be used by the glass packaging manufacture plant in Spotswood in support of Visy’s target of 70% recycled glass in new glass packaging.

- Visy and Orora continue to push up the post-consumer recycled content in glass packaging: This has increased from approximately 30–35% in 2020 to an average of a little over 40% as of 2021–22, and possibly as much as 55–60% by the first half of 2024.

Material overview and market summary

Recycling of glass packaging is an established market.

Materials used for packaging continue to evolve as brand owners respond to consumer sentiment. This may result in increased glass packaging over time, as brand owners move away from plastic. One key market player has noted a shift from plastic to glass packaging containers for some of their products.

Crushed glass, as a glass sand replacement, is growing in Victoria. This has been supported by changes to construction specifications, which have increased how much recycled glass sand can be used in road and rail construction.

Nationally it is contaminated glass collected through materials recovery facilities (MRFs) that continues to be destined for road construction or landfill remediation, as container deposit scheme (CDS) generated glass is preferred for new packaging manufacture. The demand for packaging glass-based sand replacement product is high in Victoria as it competes well on price and quality with quarried sand.

Small quantities of beneficiated glass were exported out of Victoria in early 2023. However, Victoria has not reported any glass exports since March 2023. Overall, the market for sorted glass packaging is much stronger than it has been in recent years.

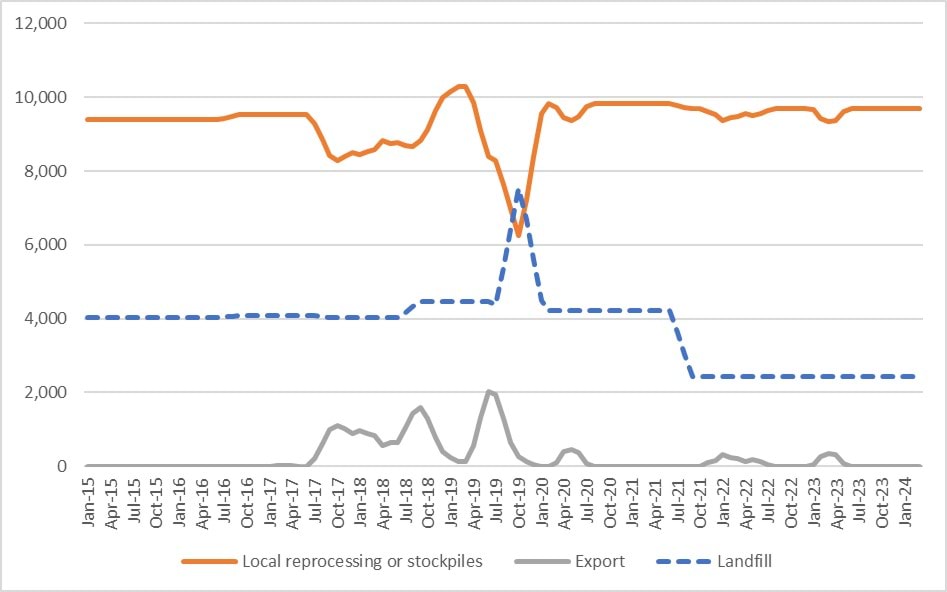

Figure 1 provides data on movements in export and local destinations of kerbside collected glass since the beginning of 2015. Exports of kerbside glass are generally low and sporadic, with minimal exports occurring since July 2020. Landfill disposal remains steady at around 2,000 tonnes per month.

Figure 1: Destination of Victorian MRF outputs (tonnes per month) – kerbside glass

{kind=link}

Prices, demand and supply

Gate fee rates for MRFs sending material for beneficiation can vary, based on quality and quantities. There has been no change in reported gate fees of $0 per tonne at the outgoing gate of the MRF (EXW MRF) to -$30 per tonne reported for glass going to beneficiation. Prices are lower if the glass is going into other applications such as road construction. Delivered MRF sorted mixed glass destined for road base or asphalt production continues to incur a gate fee that is greater than the fee into beneficiation, but less than a landfill gate fee. On average it is expected to be around -$50 to -$80 per tonne (cost to the MRF operators).

The cost of beneficiation for food grade packaging is estimated at approximately $150–$200 per tonne but is dependent on the source and processing requirement of the incoming glass. There have been no exports of beneficiated glass out of Victoria since March 2023, therefore, there is limited data on the recent exported commodity value.

Beneficiated glass was reported to customs at values of approximately $140 per tonne across January to March 2023. In Victoria, the price paid at facilities for glass cullet from beneficiation plants is believed to have remained largely unchanged in recent years.

The limited beneficiation capacity has restricted the amount of glass suitable for production. Beneficiation capacity is expanding nationally, which may address the supply–demand imbalance of recent years.

Key end markets and related specifications

While the market for used glass packaging into packaging production may fall short of national demand, there are a range of other secondary markets which may be used. These include the major market of glass into asphalt, road base material and sand for construction, and smaller markets for abrasives, and filter media. More novel markets may also emerge; however these markets will likely be small.

Export and interstate market review

Glass cullet is not exported in significant quantities due to its low value and significant weight relative to shipping costs. However, this market may develop if large quantities of high-quality beneficiated glass increase in availability. In Victoria, previous exports of glass cullet have mostly been to Malaysia or Bangladesh. While there have been no glass exports from Victoria in the 2023–24 financial year (as of March 2024), Malaysia remains a key destination for the minor amounts sent from other states and territories in Australia. From January 2021 a licence has been required for all exports of glass packaging, with unprocessed (unbeneficiated) glass not eligible for export. Large international trading markets for glass cullet do exist, most significantly in the European Union. For example, Italy is a major destination of glass cullet sourced from other countries.

Market opportunities

Beneficiation capacity is expanding nationally, which may address the supply–demand imbalance of recent years. The constrained bottle-to-bottle recycling market in Australia, with only five facilities will also play a role in the market.

As noted previously, the national glass demand (into packaging) will not be able to absorb all the packaging glass supply, even if beneficiated. As a result, significant non-packaging end markets for recovered glass will continue to be required, or export markets for the beneficiated glass could be an environmentally preferable solution.

Other end markets for the glass, such as the construction sector, may be needed even though this is a less circular solution.

Report disclaimer

The information in this report was prepared in conjunction with Blue Environment.

While reasonable efforts have been made to ensure that the contents of this publication are factually correct, Recycling Victoria gives no warranty regarding its accuracy, completeness, currency or suitability for any particular purpose and to the extent permitted by law, does not accept any liability for loss or damages incurred as a result of placed upon the content of this publication.

This publication is provided on the basis that all persons accessing it undertake responsibility for assessing the relevance and accuracy of its content.

Recycling Victoria does not accept any liability for loss or damage arising from your use of or reliance on the Data. The inclusion of information in this report does not constitute Recycling Victoria’s endorsement of any particular facility, or any associated organisation, product or service.

Accessibility disclaimer

The Victorian Government is committed to providing a website that is accessible to the widest possible audience, regardless of technology or ability.

This page contains an embedded complex image file (Figure 1) that may not meet our minimum WCAG AA Accessibility standards.

If you are unable to read any of the content of this page, you can contact the content owners for an Accessible version.

Contact email: rvdata@deeca.vic.gov.au

Updated