Notable market developments

- Prices for recovered tin-plate steel cans and aluminium beverage cans have recovered strongly over the last 2 years from the mid-2020 lows. They are trading at reasonable levels, coming off price peaks around March 2022. Prices for both tin-plate steel cans and aluminium beverage cans have decreased from the very high prices seen across the first half of 2022.

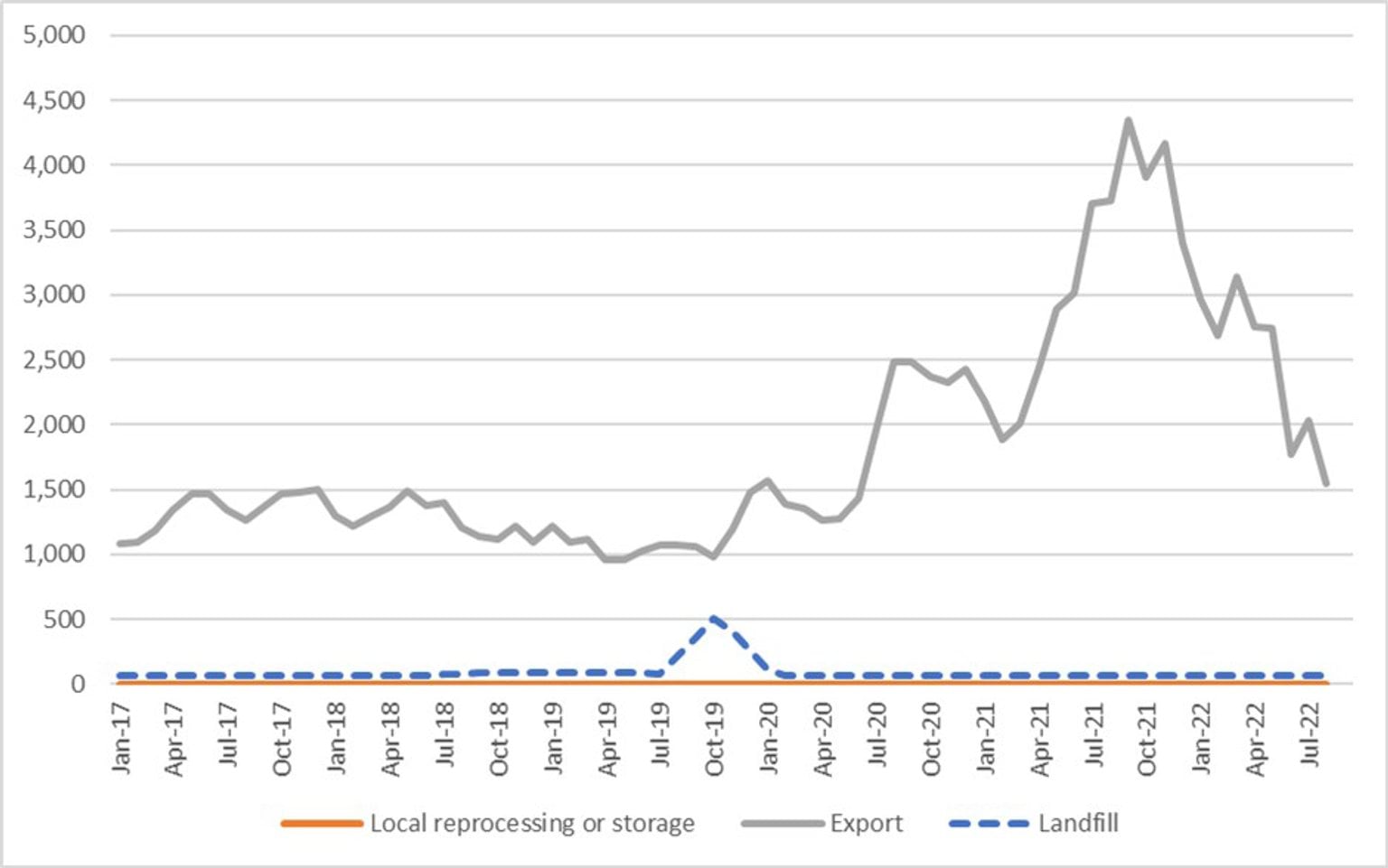

- Exports of tin-plate steel cans and aluminium beverage cans have fallen steeply since the middle of 2021 and are back near the long-term average for metal packaging exports. The high prices across the 2021–22 financial year probably reduced stockpiles of baled cans built up by material recovery facility (MRF) operators and scrap metal traders during the period of very low prices across the 2020 calendar year. This stockpile drawdown is now complete, and exports have likely stabilised at close to the level of MRF sorting with the higher prices providing little incentive to stockpile.

- Container costs were at record high prices across the second half of 2021. International freight costs have been very high since the middle of 2021 but have moderated somewhat over the July–September 2022 period. This high cost has put downward pressure on exports even though metal prices have been good to excellent. It is likely that the high freight costs are a contributor to the high metals price, as exporters have to recoup the container contract cost. They have also been able to pass a significant proportion of this cost onto overseas buyers, due in large part to the high prices for virgin aluminium and steel, and scrap aluminium and steel from non-packaging sources.

Material overview and market summary

Steel and aluminium cans, mostly recovered through household kerbside recycling collections, only account for a small fraction of overall metals recovery in Victoria.

MRFs are well equipped to separate these materials from household collections into marketable grades of recyclate, which although small in volume (around 3–4% of the average household recycling bin) represent a valuable source of revenue for MRFs.

Recovered steel packaging is considered a low value form of steel post-consumer, but is still saleable into overseas markets, sometimes by blending it into mixed grade steel products such as 'black iron'. It is not purchased by local smelter operators in any volume.

Figure 1 provides data on the change in exports of kerbside recovered metal packaging since the start of 2017. The jump in metal packaging exports from July 2020 to April 2022 is likely due to the large increase in scrap metal prices across the (approximately) same period. There were notable price increases for both tin-plate steel cans and aluminium beverage cans across the June 2021–May 2022 period, with prices decreasing somewhat to September 2022, but still at reasonable levels historically.

Figure 1: Destination of Victorian MRF outputs (tonnes per month) – metal packaging

{kind=link}

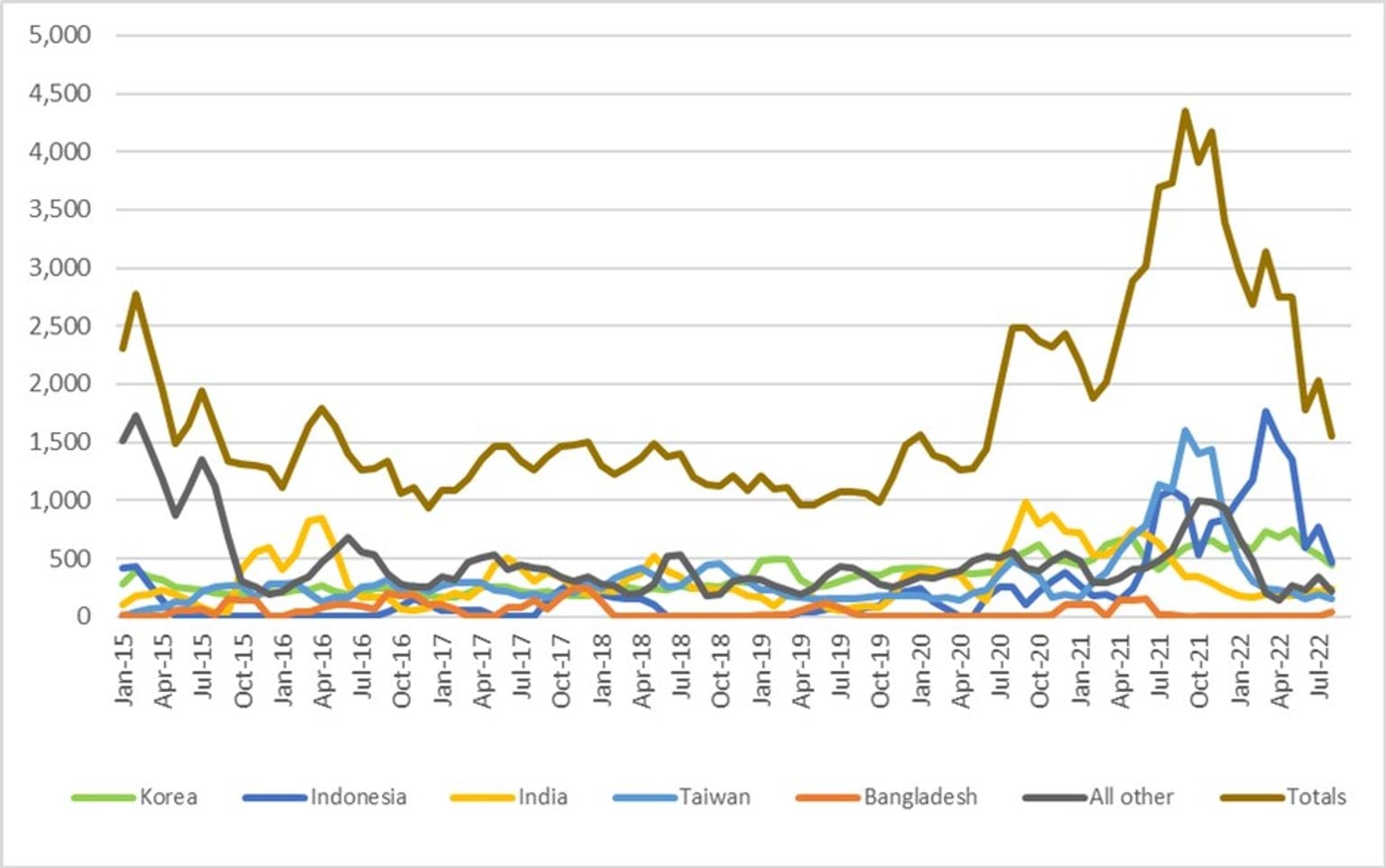

Throughout 2022, baled steel and aluminium packaging was sent to many different countries, with the main destinations being Thailand, Indonesia, South Korea, Taiwan, and India. Almost all recovered metal packaging is sold into export markets, with no Victorian tin-plated steel or aluminium packaging identified as being reprocessed in Australia. This is reportedly due to the much better export prices on offer, relative to local interest and prices.

There are trials of small quantities of tin-plated and aluminium packaging reported as reprocessed in other states, and it is expected that these quantities will increase over coming years.

Prices, demand and supply

While there is currently little steel or aluminium packaging post-consumer reprocessed in Australia, international markets for these commodities remain strong.

There are 2 aluminium smelter operators in Australia that are reportedly investigating upgrading their facilities to take used aluminium beverage cans. These are in Tasmania and Queensland. This may provide some increased surety of local reprocessing capacity, and a buffer from international trading conditions, should they deteriorate.

There is no reported significant distressed storage of steel or aluminium packaging, which the jump in exports over the last 12 months supports.

The price of steel packaging is strongly linked to global steel pricing. The current price (September 2022) received for baled steel packaging is around $350–$400 per tonne (Ex Works (EXW) MRF). This illustrates strong growth from the price of around $90–$100 per tonne seen back in the middle of 2020.

The price of shipped aluminium packaging is linked to virgin aluminium pricing. The current price (September 2022) received for baled aluminium beverage cans is approximately $2,200–$2,300 per tonne (EXW MRF). This is strong growth from the price of around $800–$900 per tonne seen back in the middle of 2020.

Key end markets and related specifications

Exported steel packaging has specifications relating to contamination levels and bale density. The sorting that is undertaken at MRFs allows the baled material to meet these specifications without major difficulty or manual sorting input. A similar situation exists for aluminium packaging.

Generally steel and aluminium packaging is recycled back into the respective post-consumer metal pools and go into durable applications such as vehicles, building materials and many other products.

Export and interstate market review

The exported steel and aluminium packaging is sold into large markets with most metal coming from non-packaging sources. The material flows from all countries and is destined for wherever the demand requires material for production. Unlike some other materials, there is no way of knowing the origin of the steel or aluminium in new product. Demand and pricing can increase or decrease based on worldwide supply and demand conditions.

Exports of kerbside recovered metal packaging have increased to a high level since June 2020, driven by a sharp return in exports to India (which has now fallen away), increases in exports to Taiwan, South Korea, and Indonesia, and continually improving prices across 2021 and the first half of 2022. The fall from October 2021 may be due to the completion of the drawdown of stockpiled bales, and some slowdown in exports due to supply chain disruptions and very high container costs over the second half of 2021 and 2022.

Figure 2: Victorian recovered kerbside metal packaging, to export country (tonnes per month)

{kind=link}

Prior to the pandemic and the current tight market for containers, the typical 12 month contracted price for 50 twenty-foot container movements to southeast Asia, with a capacity of 20 tonnes each, was in the order of $USD300 per container, and was even much lower for scrap material movements (which received lower ‘back hauling’ prices), which were in the order of $USD100–200 per container.

Back hauling pricing has reportedly dried up and this same contract is reportedly in the order of $USD2700–3500 per container, with no reduced price for scrap materials. For high value metals like aluminium, this huge price increase is less critical, but for steel cans it represents a very significant cost input increase for exporters. Onshore smelting of steel cans would avoid this cost risk. However, some degree of local preliminary reprocessing of tin-plate steel cans, for example in a hammer-mill to reduce contamination, may be required to make tin-plate steel packaging more attractive to local smelter operators.

Given the relaxation of COVID-19 restrictions in China and many manufacturers playing catchup on freight movements, and the typical increase in freight movements at the end of the year, container costs are likely to remain high into 2023.

It is also worth noting that there is little container freight provider competition from Australia to the major destinations for scrap metal packaging, and it is possible that there are collusive price practices occurring, a practice that the Australian Competition and Consumer Commission, along with US, Canadian, New Zealand and UK governments have recognised as a possibly serious problem globally.

Table 1: Annual Victorian recovered kerbside recovered metals, to export country (tonnes per year).

| Country* | 2015–16 (tonnes) | 2016–17 (tonnes) | 2017–18 (tonnes) | 2018–19 (tonnes) | 2019–20 (tonnes) | 2020–21 (tonnes) | 2021–22 (tonnes) | 2022–23** (tonnes) |

|---|---|---|---|---|---|---|---|---|

Country* Indonesia | 2015–16 (tonnes) 0 | 2016–17 (tonnes) 600 | 2017–18 (tonnes) 1,700 | 2018–19 (tonnes) 200 | 2019–20 (tonnes) 1,300 | 2020–21 (tonnes) 3,000 | 2021–22 (tonnes) 12,700 | 2022–23** (tonnes) 1,200 |

Country* Korea | 2015–16 (tonnes) 2,600 | 2016–17 (tonnes) 2,600 | 2017–18 (tonnes) 2,600 | 2018–19 (tonnes) 3,900 | 2019–20 (tonnes) 4,500 | 2020–21 (tonnes) 6,400 | 2021–22 (tonnes) 7,300 | 2022–23** (tonnes) 1,000 |

Country* India | 2015–16 (tonnes) 5,200 | 2016–17 (tonnes) 2,400 | 2017–18 (tonnes) 4,000 | 2018–19 (tonnes) 2,400 | 2019–20 (tonnes) 2,700 | 2020–21 (tonnes) 8,400 | 2021–22 (tonnes) 3,400 | 2022–23** (tonnes) 500 |

Country* Taiwan | 2015–16 (tonnes) 2,700 | 2016–17 (tonnes) 3,100 | 2017–18 (tonnes) 3,200 | 2018–19 (tonnes) 3,300 | 2019–20 (tonnes) 2,100 | 2020–21 (tonnes) 4,800 | 2021–22 (tonnes) 9,100 | 2022–23** (tonnes) 300 |

Country* Bangladesh | 2015–16 (tonnes) 900 | 2016–17 (tonnes) 1,100 | 2017–18 (tonnes) 1,100 | 2018–19 (tonnes) 300 | 2019–20 (tonnes) 100 | 2020–21 (tonnes) 800 | 2021–22 (tonnes) 0 | 2022–23** (tonnes) 0 |

Country* All other | 2015–16 (tonnes) 6,500 | 2016–17 (tonnes) 4,800 | 2017–18 (tonnes) 4,000 | 2018–19 (tonnes) 3,500 | 2019–20 (tonnes) 4,500 | 2020–21 (tonnes) 5,100 | 2021–22 (tonnes) 6,700 | 2022–23** (tonnes) 600 |

Country* Total | 2015–16 (tonnes) 17,900 | 2016–17 (tonnes) 14,600 | 2017–18 (tonnes) 16,600 | 2018–19 (tonnes) 13,600 | 2019–20 (tonnes) 15,200 | 2020–21 (tonnes) 28,500 | 2021–22 (tonnes) 39,200 | 2022–23** (tonnes) 3,600 |

Source: ABS and IE (Australian Harmonized Export Commodity Classification (AHECC) data by month, classification, and destination country, 2022) and Blue Environment.

* Countries ranked by average of last 3 months of exports.

** Partial year across July 2022 to August 2022.

Table 2: Example monthly change in Victorian recovered metals, to export country (tonnes per month).

| Country | July 2022 (tonnes) | August 2022 (tonnes) | Change (%) |

|---|---|---|---|

Country Indonesia | July 2022 (tonnes) 800 | August 2022 (tonnes) 500 | Change (%) -38% |

Country Korea | July 2022 (tonnes) 500 | August 2022 (tonnes) 400 | Change (%) -20% |

Country India | July 2022 (tonnes) 200 | August 2022 (tonnes) 200 | Change (%) 0% |

Country Taiwan | July 2022 (tonnes) 200 | August 2022 (tonnes) 100 | Change (%) -50% |

Country Bangladesh | July 2022 (tonnes) 0 | August 2022 (tonnes) 0 | Change (%) N/A |

Country All other | July 2022 (tonnes) 300 | August 2022 (tonnes) 200 | Change (%) -33% |

Country Total | July 2022 (tonnes) 2,000 | August 2022 (tonnes) 1,400 | Change (%) -30% |

Source: ABS and IE (Australian Harmonized Export Commodity Classification (AHECC) data by month, classification, and destination country, 2022) and Blue Environment.

Market opportunities

The global steel and aluminium markets have been able to consistently absorb metal packaging from kerbside collections, better than the local or global markets for any of the other packaging materials. This is primarily due to the lack of barriers in returning MRF sourced metal packaging back into the global scrap pool and then into many steel and aluminium products beyond packaging.

Tin-plate steel packaging is only reprocessed in very small quantities and has relatively low value, with reports of high levels of contamination. There is an increasing risk of future import restrictions by receiving countries, particularly if mixed grade post-consumer steel imports such as 'black iron' scrap grades are restricted for any reason, as tin-plate steel is often 'shandied' (blended) into other scrap steel grades to enable its sale. There may be a case for Australian governments to assess the potential for local pre-processing capacity here in Australia, such as hammer-mills to decontaminate the tin-plate steel to make it more attractive to local and international smelter operators.

In addition, the increasing costs of container freight present a risk to steel cans exporters in getting this material to smelters in southeast Asia.

If there was a dramatic negative shift in supply/demand at a global level, in tandem with the current very high freight costs, this could lead to significant price reductions for baled steel, which would leave this material stranded in Australia with minimal local reprocessing capacity.

Report disclaimer

The information on this report was prepared in conjunction with Blue Environment, IndustryEdge and Sustainable Resource Use (SRU).

While reasonable efforts have been made to ensure that the contents of this publication are factually correct, Recycling Victoria gives no warranty regarding its accuracy, completeness, currency, or suitability for any particular purpose and to the extent permitted by law, does not accept any liability for loss or damages incurred as a result of placed upon the content of this publication.

This publication is provided on the basis that all persons accessing it undertake responsibility for assessing the relevance and accuracy of its content.

Recycling Victoria does not accept any liability for loss or damage arising from your use of or reliance on the data. The inclusion of information in this report does not constitute Recycling Victoria’s endorsement of any facility, or any associated organisation, product or service.

Accessibility disclaimer

The Victorian Government is committed to providing a website that is accessible to the widest possible audience, regardless of technology or ability.

This page contains two embedded complex image files (Figures 1 and 2) that may not meet our minimum WCAG AA Accessibility standards.

If you are unable to read any of the content of this page, you can contact the content owners for an Accessible version.

Contact email: rvdata@delwp.vic.gov.au

Updated