June 2024

Notable market developments

- Global pulp prices returned to strong growth in early 2024 as supply-side challenges impacted all fibre costs.

- Mixed recovered paper prices have increased in the first half of 2024.

- Local market conditions have stabilised, supplemented by exports, with new retail-focused products made from recovered fibre absorbing some volumes.

- Impending introduction of export licencing for fibre has caused limited practical impact to date, with no observable or expected market disruptions.

Material overview and market summary

Australia’s recovered paper exports lifted almost 7% over the year-ending March 2024, reaching 1.093 million tonnes. Victoria’s exports were broadly in line with the national growth, rising 8% to 0.3 million tonnes or around 28% of total national exports for the same period.

Demand from the main market, Indonesia, continues to be relatively strong, as there has been some resurgence in industrial demand for packaging materials in Southeast Asia and China. A driver for this has been China’s fiscal stimulus, and significantly, the continued upwards pressure on virgin fibre pulp prices which has led to packaging producers looking to secondary and alternative fibres when substitution is an option.

The relatively tight balances for fibre supplies are an important feature of this market dynamic. Pulp supply disruptions due to industrial action in Finland and Chile resulted in major pulp users experiencing a sharp fall in inventories. With limited additional supply available, pulp prices lifted steeply from March to June 2024. The price increases were not matched for the paper and board products manufactured from the pulp, resulting in increased demand and prices for recovered paper.

It is widely reported that global industrial production has been stagnant over the last two years, a result of reduced expenditure amidst strong inflation and broad cost-of-living pressures. This has in turn reduced the volume of recovered paper being generated in many net-exporting countries, including Australia.

Industry participants suggest the marginal additional export supply from Australia (less than 70,000 tonnes for the year-ended April) is not directly linked to softer demand for recovered paper domestically. As one exporter said, across the year, this additional volume is no more than an inventory adjustment.

Domestic demand remains stable, albeit slightly muted by local consumption pressures.

An emerging factor for demand for recovered fibre is the alternative and retail focussed products being progressively introduced as replacements for soft plastics and as part of moves toward circular economy principles. The recent launch of Visy Tread, manufactured entirely from recovered paper, is an example of alternative industrial demand which can be expected to increase in coming years.

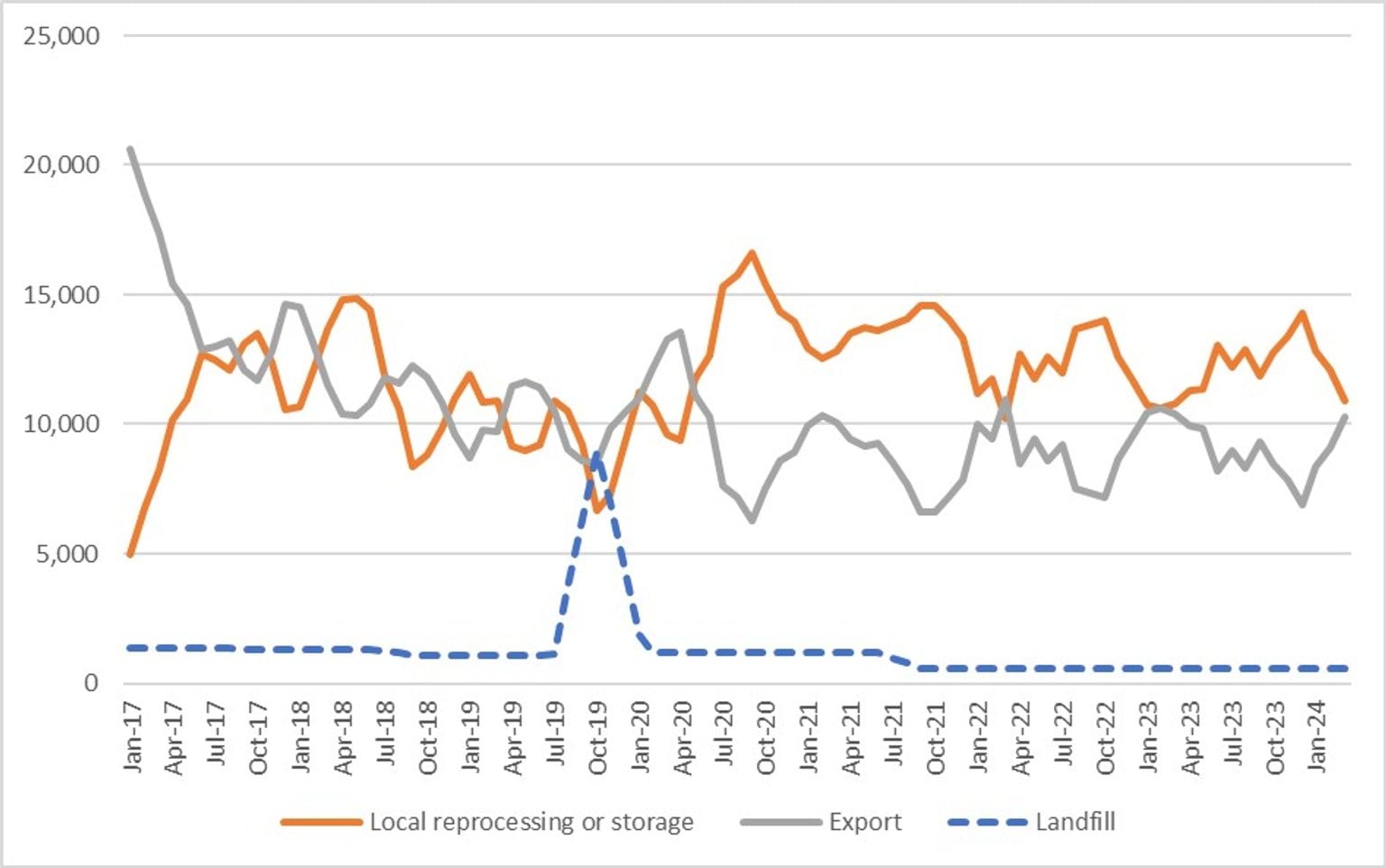

Figure 1: Destination of Victorian material recovery facility (MRF) outputs (tonnes per month) – kerbside paper and paperboard

{kind=link}

Prices, demand and supply

To the end of March 2024, global fibre prices lifted sharply, amidst supply-side and related substitution pressures. When global virgin pulp prices rise to the point where major paper and board manufacturers cannot recover their costs, alternative fibres will be more sought after and their prices will rise. This is especially the case for higher quality and reliable supply, such as Australia’s supply.

In Australian markets the global price dynamic has been reflected in general, but with some variation for best quality Old Corrugated Cartons (OCC), for which there is consistent demand.

Key end markets and related specifications

There are no new end markets for kerbside recovered paper, despite increased attention on a small number of solutions.

The only application to take a wide range and large volume of recovered paper is corrugated packaging. Australia is largely self-sufficient and a net exporter, with capacity to recycle greater than domestic consumption.

Export and interstate market review

Victoria’s exports of mixed recovered paper have lifted close to 132,000 tonnes per annum, accounting for close to 44.3% of total Victorian annual exports to the end of March 2024.

Interstate trade flows of recovered paper have reportedly increased since early 2024, but market participants were unable to pinpoint exact volumes. However, they were able to identify that improved prices in the first quarter of 2024 were encouraging increased interstate transfers and flowing on to increased exports.

In Victoria, regardless of the state of origin, mixed recovered paper is more to be reprocessed domestically, while the ‘clean’ or pure OCC grade (AHECC 4707.1) is more likely to be exported.

Some industry participants have argued increased exports are part of an effort by some exporters to exit stock prior to 1 July 2024 when the export regulations and licencing requirements commence. There is however no objective evidence for this and there is no evidence of reduced pricing which would follow such a move. Weighted average export prices have increased and detailed examination demonstrates there are no ‘fire sale’ prices evident in export transactions.

The export licencing regime is currently being implemented, on the phased basis set out in the Regulations.

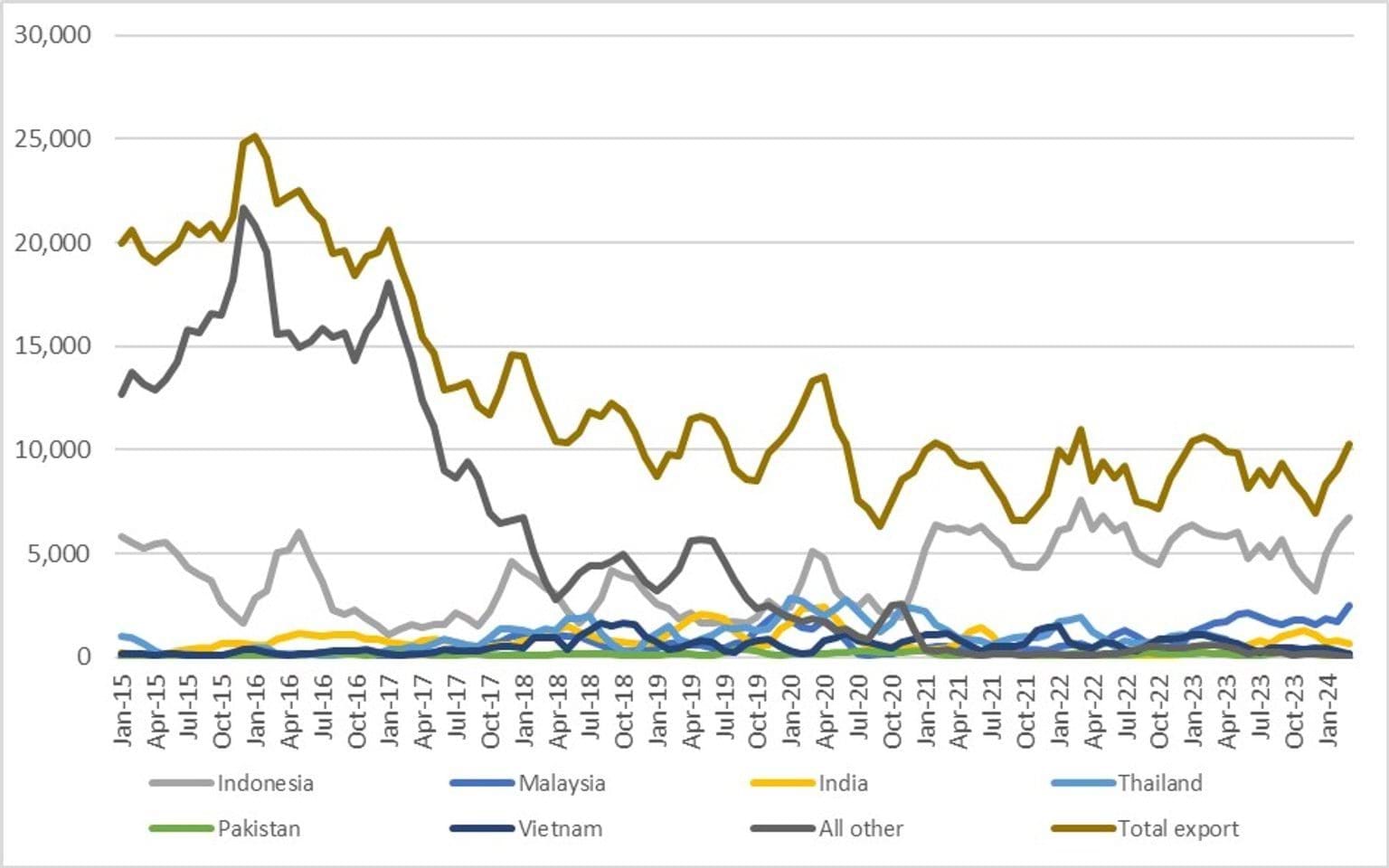

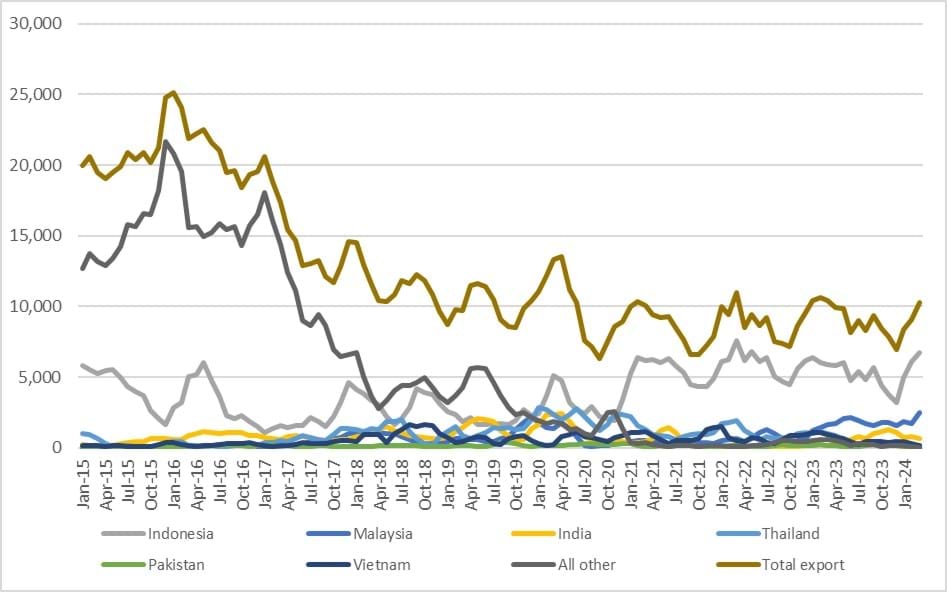

Indonesia remains the main destination for Victoria’s (and Australia’s and New Zealand’s) recovered paper, especially the kerbside collected volumes. Proximity and relationships are driving this continued trade, but notably, India and Malaysia now have a strong presence in the national market for kerbside collected volumes.

Figure 2: Victorian recovered kerbside paper and paperboard, to export country (tonnes per month)

{kind=link}

Table 1: Annual Victorian recovered kerbside paper and paperboard, to export country

| Country* | 2015–16 (tonnes) | 2016–17 (tonnes) | 2017–18 (tonnes) | 2018–19 (tonnes) | 2019–20 (tonnes) | 2020–21 (tonnes) | 2021–22 (tonnes) | 2022–23 (tonnes) | 2023-24** (tonnes) |

|---|---|---|---|---|---|---|---|---|---|

Country* Indonesia | 2015–16 (tonnes) 45,000 | 2016–17 (tonnes) 22,000 | 2017–18 (tonnes) 34,000 | 2018–19 (tonnes) 32,000 | 2019–20 (tonnes) 34,000 | 2020–21 (tonnes) 51,000 | 2021–22 (tonnes) 68,000 | 2022–23 (tonnes) 67,000 | 2023-24** (tonnes) 45,000 |

Country* Malaysia | 2015–16 (tonnes) 1,000 | 2016–17 (tonnes) 2,000 | 2017–18 (tonnes) 10,000 | 2018–19 (tonnes) 6,000 | 2019–20 (tonnes) 16,000 | 2020–21 (tonnes) 4,000 | 2021–22 (tonnes) 6,000 | 2022–23 (tonnes) 15,000 | 2023-24** (tonnes) 16,000 |

Country* India | 2015–16 (tonnes) 8,000 | 2016–17 (tonnes) 10,000 | 2017–18 (tonnes) 10,000 | 2018–19 (tonnes) 14,000 | 2019–20 (tonnes) 18,000 | 2020–21 (tonnes) 8,000 | 2021–22 (tonnes) 2,000 | 2022–23 (tonnes) 2,000 | 2023-24** (tonnes) 8,000 |

Country* Thailand | 2015–16 (tonnes) 2,000 | 2016–17 (tonnes) 4,000 | 2017–18 (tonnes) 14,000 | 2018–19 (tonnes) 11,000 | 2019–20 (tonnes) 24,000 | 2020–21 (tonnes) 19,000 | 2021–22 (tonnes) 13,000 | 2022–23 (tonnes) 9,000 | 2023-24** (tonnes) 3,000 |

Country* Pakistan | 2015–16 (tonnes) 1,000 | 2016–17 (tonnes) 2,000 | 2017–18 (tonnes) 1,000 | 2018–19 (tonnes) 1,000 | 2019–20 (tonnes) 2,000 | 2020–21 (tonnes) 2,000 | 2021–22 (tonnes) 1,000 | 2022–23 (tonnes) 2,000 | 2023-24** (tonnes) 1,000 |

Country* Vietnam | 2015–16 (tonnes) 2,000 | 2016–17 (tonnes) 3,000 | 2017–18 (tonnes) 7,000 | 2018–19 (tonnes) 12,000 | 2019–20 (tonnes) 7,000 | 2020–21 (tonnes) 9,000 | 2021–22 (tonnes) 9,000 | 2022–23 (tonnes) 9,000 | 2023-24** (tonnes) 3,000 |

Country* All other | 2015–16 (tonnes) 206,000 | 2016–17 (tonnes) 175,000 | 2017–18 (tonnes) 72,000 | 2018–19 (tonnes) 54,000 | 2019–20 (tonnes) 28,000 | 2020–21 (tonnes) 11,000 | 2021–22 (tonnes) 1,000 | 2022–23 (tonnes) 5,000 | 2023-24** (tonnes) 1,000 |

Country* Total | 2015–16 (tonnes) 265,000 | 2016–17 (tonnes) 218,000 | 2017–18 (tonnes) 148,000 | 2018–19 (tonnes) 130,000 | 2019–20 (tonnes) 129,000 | 2020–21 (tonnes) 104,000 | 2021–22 (tonnes) 100,000 | 2022–23 (tonnes) 109,000 | 2023-24** (tonnes) 77,000 |

Source: ABS and IE (Australian Harmonized Export Commodity Classification (AHECC) data by month, classification and destination country, 2024) and Blue Environment.

* Countries ranked by average of last 3 months of exports.

** Partial year across July 2023 to March 2024.

Table 2: Example monthly change in Victorian recovered kerbside paper and paperboard, to export country

| Country | February 2024 (tonnes) | March 2024 (tonnes) | Change (%) |

|---|---|---|---|

Country Indonesia | February 2024 (tonnes) 6,100 | March 2024 (tonnes) 6,700 | Change (%) 10% |

Country Malaysia | February 2024 (tonnes) 1,700 | March 2024 (tonnes) 2,500 | Change (%) 47% |

Country India | February 2024 (tonnes) 800 | March 2024 (tonnes) 700 | Change (%) -13% |

Country Thailand | February 2024 (tonnes) 100 | March 2024 (tonnes) 200 | Change (%) 100% |

Country Pakistan | February 2024 (tonnes) 100 | March 2024 (tonnes) 100 | Change (%) 0% |

Country Vietnam | February 2024 (tonnes) 300 | March 2024 (tonnes) 100 | Change (%) -67% |

Country All other | February 2024 (tonnes) 100 | March 2024 (tonnes) 0 | Change (%) -100% |

Country Total | February 2024 (tonnes) 9,200 | March 2024 (tonnes) 10,300 | Change (%) 12% |

Market opportunities

While the impact of the export licencing regime is expected to be minimal from the middle of 2024, major opportunities continue to be domestically focussed. New products reduce the reliance on exports of recyclable material and increases domestic self-sufficiency, to a greater or lesser extent.

Supply chain consolidations and market adjustments continue to be likely because of export licencing for mixed recovered paper. Exports ensure fibre is being recycled, usually into (recyclable) corrugated packaging. This is a more desirable outcome than destruction of the fibre through composting or use in energy from waste production.

Report disclaimer

The information in this report was prepared in conjunction with IndustryEdge and Blue Environment.

While reasonable efforts have been made to ensure that the contents of this publication are factually correct, Recycling Victoria gives no warranty regarding its accuracy, completeness, currency or suitability for any particular purpose and to the extent permitted by law, does not accept any liability for loss or damages incurred as a result of placed upon the content of this publication.

This publication is provided on the basis that all persons accessing it undertake responsibility for assessing the relevance and accuracy of its content.

Recycling Victoria does not accept any liability for loss or damage arising from your use of or reliance on the data. The inclusion of information in this report does not constitute Recycling Victoria’s endorsement of any particular facility, or any associated organisation, product, or service.

Accessibility disclaimer

The Victorian Government is committed to providing a website that is accessible to the widest possible audience, regardless of technology or ability.

This page contains two embedded complex image files (Figures 1 and 2) that may not meet our minimum WCAG AA Accessibility standards.

If you are unable to read any of the content of this page, you can contact the content owners for an accessible version.

Contact email: rvdata@deeca.vic.gov.au

Updated