Notable market developments

- Prices for recovered high-density polyethylene (HDPE) bottles have remained at a high level across 2021 and most of 2022 but appear to be trending down from August 2022. Packaging scrap prices for natural HDPE, such as milk bottles, have been very strong for nearly 18 months now, and the material is highly sought after locally and overseas. However, from 1 July 2022 the recycled HDPE (rHDPE) must be flaked and washed to be exported, which is possibly putting downward pressure on unprocessed bale prices as local reprocessing capacity catches up with the available local supply.

- Prices for recovered polyethylene terephthalate (PET) bottles have come off the highs of the middle of 2022 and appear to be trending down from August 2022. PET packaging scrap prices have decreased from around $1,100–$1,200 per tonne in the middle of the year, to around $550–$650 per tonne in September 2022. Since 1 July 2022, recycled (rPET) must be flaked and washed to be exported, which is possibly putting downward pressure on unprocessed bale prices as local reprocessing capacity catches up with the available local supply.

- Export prices for food-grade rPET and rHDPE continue to be significantly higher than virgin resin prices. Brand owners internationally are demanding recycled content for their packaging, to meet corporate commitments on recycled content targets. As unprocessed plastics cannot be exported from Australia from 1 July 2022, local reprocessors of scrap plastics, that meet the export quality thresholds, will have deep end-markets for their production for the foreseeable future.

- Plastics reprocessors are under labour availability and cost pressures. Numerous local plastic packaging reprocessors are seeking to significantly increase throughput. However, they are facing significant issues with accessing skilled labour, as well as increased electricity and transport costs.

- There are a handful of advanced (chemical) recycling projects nationally that are likely to come into operation in the 2023–2025 period. There is now around 300,000 tonnes per year of chemical recycling capacity likely to be operating in Australia by 2025, and possibly as much as 600,000 tonnes per year. These facilities will target the flexible plastic packaging generated by households, along with other non-kerbside related scrap plastics.

Material overview and market summary

Plastics collected through kerbside collections are generally sent to material recovery facilities (MRFs) and sorted from commingled recycling into a single mixed plastics grade (1–7 plastic-polymer mix), or more commonly, three or four grades, which are PET, HDPE and the residual mixed plastics grade (a 3–7 plastic-polymer mix, but with some residual quantities of PET and HDPE still present).

Two of the three major Victorian MRF operators are also positively sorting a PP stream, which is a highly sought-after product, and nationally all the major MRF operators are understood to be moving towards sorting a PP stream. Typically, the recovered PP is not reused in consumer packaging, but is incorporated into more durable goods such as plant pots.

PVC and PS are now being proactively phased out from use in packaging by many brand owners, and the quantities of these polymers in kerbside collections are already low and continue to fall. This is discussed in more detail below.

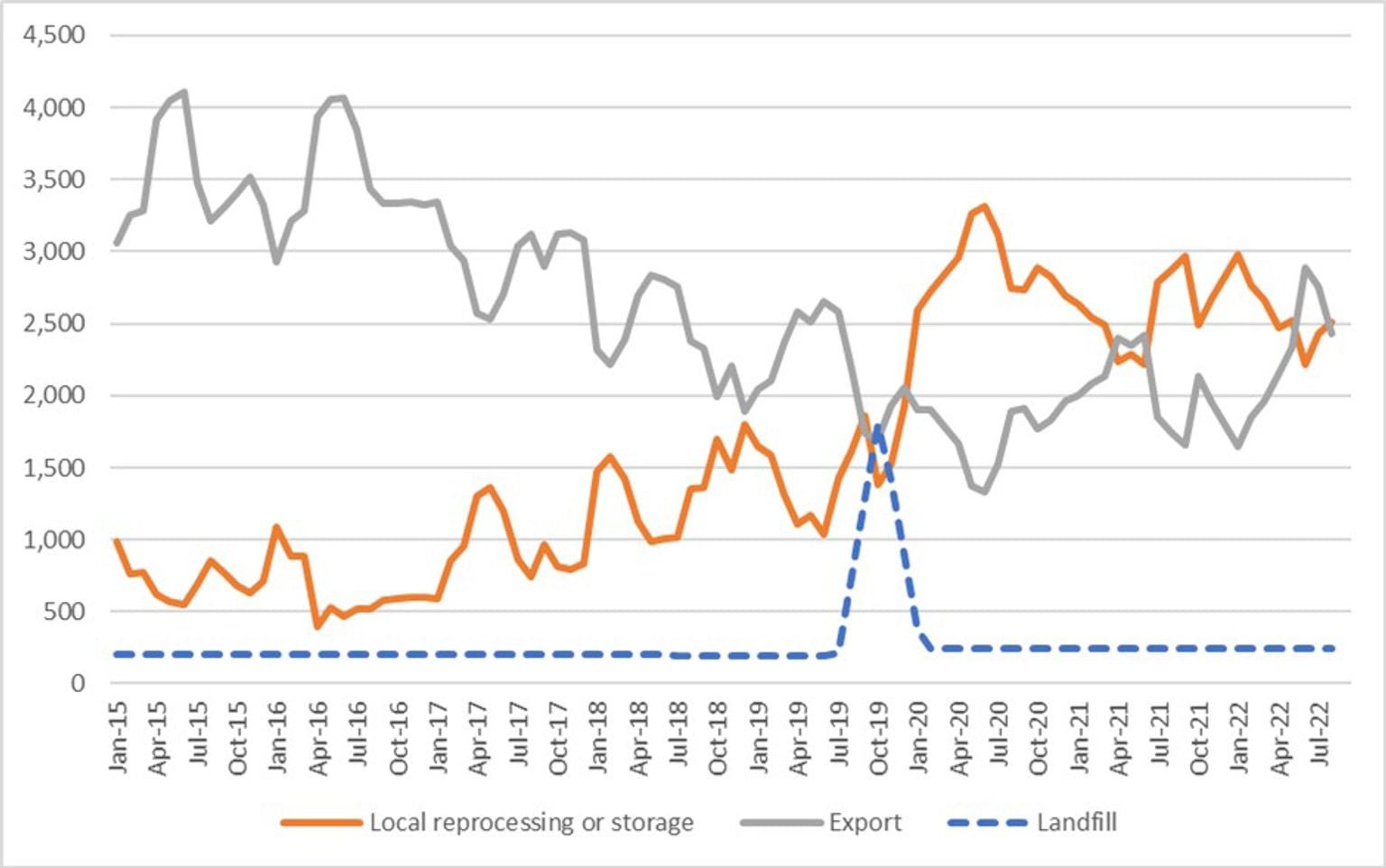

Figure 1 provides data on the change in exports of kerbside recovered plastic packaging since the beginning of 2015. There has been a steady upward trend in exports across the second half of 2020 through to around March 2022. Across the April–June 2022 period there was a significant jump in exports, possibly in preparation for the 1 July 2022 export ban on unprocessed single-polymer scrap plastics.

From 1 July 2021, the first round of Australian scrap plastic export restrictions came into force. These restrict the export of plastics to those that have been either:

- sorted into a single resin or polymer type

- processed with other materials into processed engineered fuel (PEF) (not currently exported from Victoria).

The impact of these export restrictions is visible in the export data with drops in the July 2021 and July/August 2022 exports. Further analysis of the impact of the 1 July 2022 export ban will be undertaken in the next bulletin, once the export data picture is clearer.

There are unconfirmed reports that temporary export ban exemptions have been requested by exporters and may be provided for the export of some unprocessed scrap plastic commodities, that are sought-after overseas, and for which local reprocessing capacity is not yet sufficient (in particular, commercial and industrial (C&I) sourced low-density polyethylene pallet wrap film). The main kerbside related examples of this are bales of PET or HDPE bottles.

Figure 1: Destination of Victorian MRF outputs (tonnes per month) – kerbside plastic packaging

{kind=link}

Prices, demand and supply

There continues to be strong local and export markets for clean PET bales that are collected and sorted to specification. Prices had fallen to around $230 per tonne in October 2020, the lowest price for perhaps a decade. However, prices increased steadily from this low to around $1,200–$1,300 per tonne by May 2022 (the best prices since 2017 at least). Since May 2022 prices have again softened to around $550–$650 per tonne in September 2022.

There is also increasing development of vertical supply chains in Australia by some large recycling companies and consortia, meaning that they manage their own material from collection to remanufacturing. Visy and Pact Group have these arrangements in place, and they will continue to expand. The open market prices above are not reflective of the internal transfer prices within these vertical supply chains.

The price of recycled resin used to be directly linked to the price for virgin resin. However, there is increasing 'decoupling' of the virgin PET and recycled PET (rPET) prices that has been observed over the last 2–3 years, as brand owners chase packaging grade rPET and rHDPE to meet targets on the use of recycled content in packaging. Food-grade rPET, that is virgin equivalent, is now commanding prices between 50% and 150% greater than virgin PET on global markets, and it’s reported to be often at the higher end of that range.

Prices for clean HPDE bales were around $900–$1,000 per tonne at the beginning of 2022, and then increased to $1,200–$1,300 per tonne by May 2022. Prices have fallen from these highs to around $900–$1,000 per tonne by the end of September 2022. High prices may be sustained across 2022, underpinned by the very strong local and international brand owner demand for packaging grade rHDPE. However, as stated above, the requirement to reprocessing the HDPE locally is putting downwards pressure on the price of unprocessed HDPE packaging bales.

As with reprocessed rPET, reprocessed rHDPE, that is virgin equivalent, is now commanding prices between 50% and 150% greater than virgin HDPE on global markets.

Key end markets and related specifications

Exported plastics packaging has specifications relating mostly to contamination levels. The sorting of PET, HDPE and PP undertaken at MRFs allows the baled material to generally meet these specifications without major difficulty or manual sorting input. However, as outlined above, as of July 2022 these single polymer sorted bales need to be reprocessed (chipped and washed at a minimum) to be exportable under the bans.

Export and interstate market review

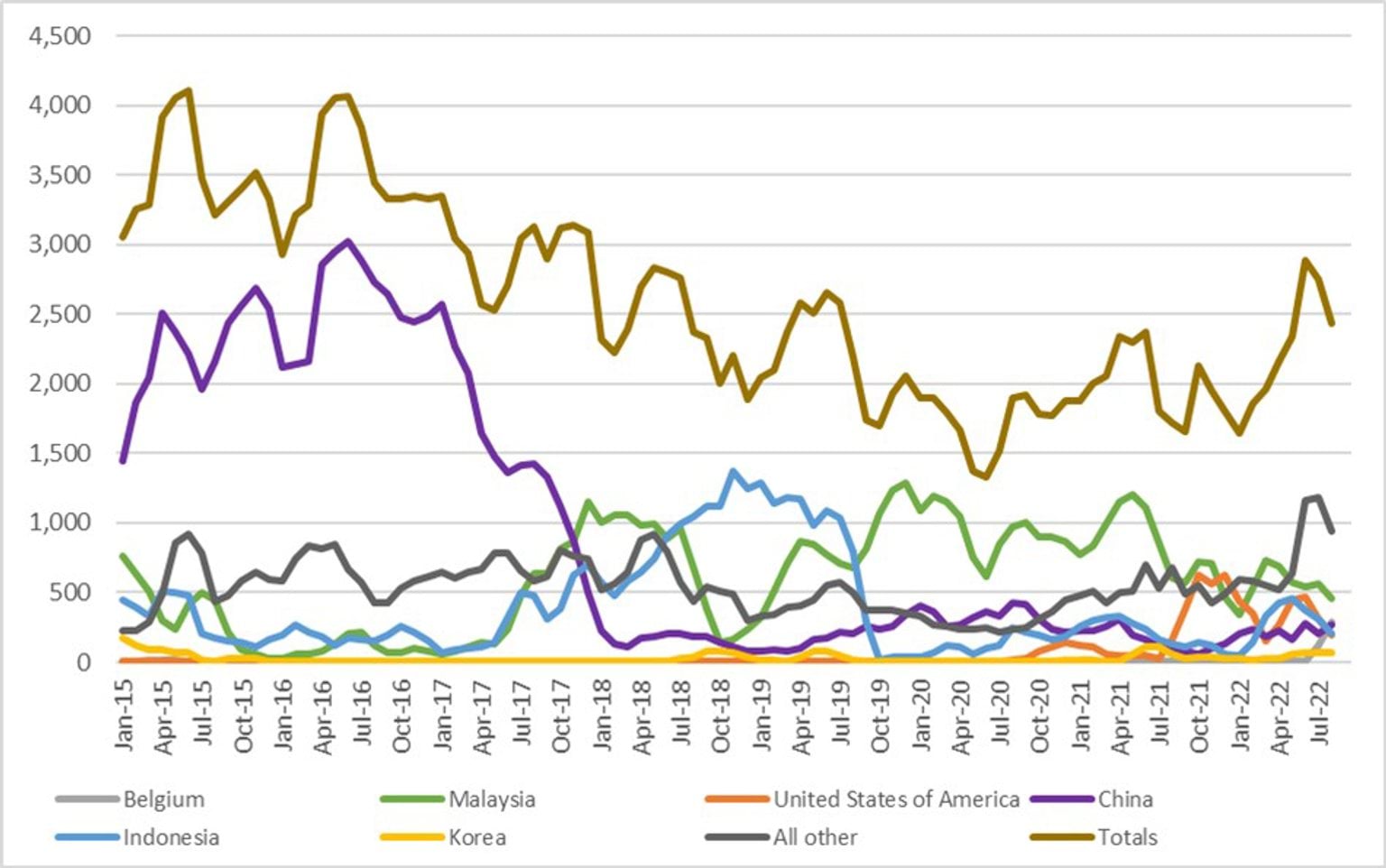

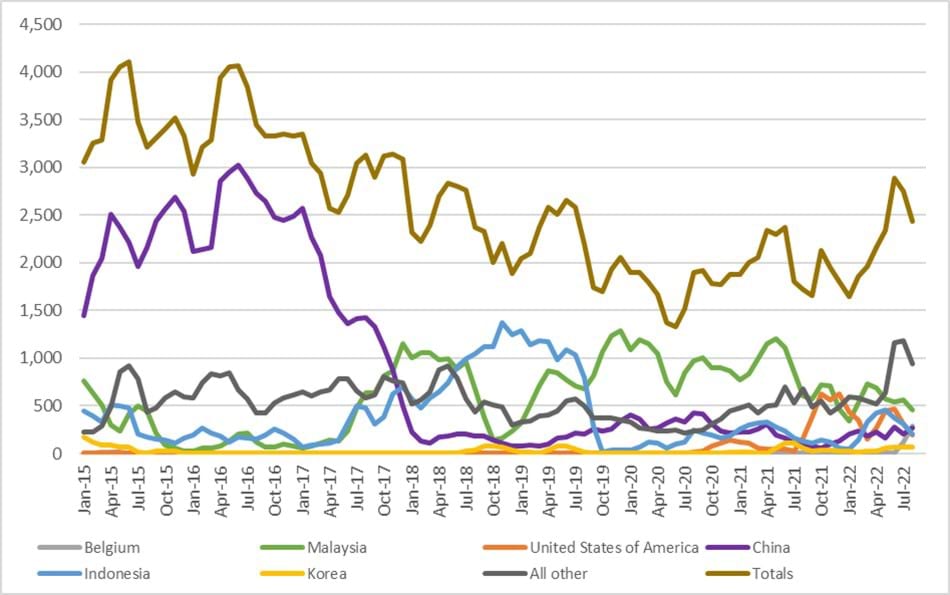

Plastics packaging was overwhelmingly exported to China (see Figure 2), until the latest round of Chinese restrictions in 2018. During the 2018–19 financial year Indonesia was the major destination. Since September 2019 Malaysia has usually been the largest destination for Victoria kerbside plastics by a significant margin.

Interestingly, exports to the USA have grown significantly since October 2021. This material is entirely rPET and rHDPE, and its trade is probably being driven by the increasing recycled content targets of brand owners in the US.

Post-consumer plastic imports into Malaysia from Victoria were fairly steady since the beginning of 2019 to August 2022, averaging around 700–900 tonnes each month, albeit with a fair degree of month-to-month variability. Exports to Indonesia have also popped up somewhat over the first half of 2022 but declined across July and August 2022.

The loss of the Chinese markets in 2017, and the saturation and restriction of imports into Indonesia (albeit with signs of recovery) has left Victoria highly exposed to Malaysian import conditions, albeit at a lower level than the historical level of exposure to China. The possible emergence of new overseas markets, such as the US and Brazil, is an encouraging development to be watched.

Regardless, the export bans now in force since July 2022 have largely ended the export of any unprocessed plastics. The kerbside plastic packaging recovery market bottleneck will shortly become onshore reprocessing capacity for PET, HPDE and PP. However, there are numerous significant new reprocessing facilities that have been announced over the last couple of years, with much of this new capacity to be located in Victoria (see Table 1).

Figure 2: Victorian recovered kerbside plastic packaging, export country (tonnes per month)

{kind=link}

Table 1: Annual Victorian recovered kerbside plastic packaging, to export country (tonnes per year).

| Country* | 2015–16 (tonnes) | 2016–17 (tonnes) | 2017–18 (tonnes) | 2018–19 (tonnes) | 2019–20 (tonnes) | 2020–21 (tonnes) | 2021–22 (tonnes) | 2022–23** (tonnes) |

|---|---|---|---|---|---|---|---|---|

Country* Malaysia | 2015–16 (tonnes) 1,900 | 2016–17 (tonnes) 1,400 | 2017–18 (tonnes) 10,600 | 2018–19 (tonnes) 6,600 | 2019–20 (tonnes) 11,600 | 2020–21 (tonnes) 11,600 | 2021–22 (tonnes) 8,400 | 2022–23** (tonnes) 1,000 |

Country* USA | 2015–16 (tonnes) 0 | 2016–17 (tonnes) 0 | 2017–18 (tonnes) 0 | 2018–19 (tonnes) 0 | 2019–20 (tonnes) 100 | 2020–21 (tonnes) 800 | 2021–22 (tonnes) 4,900 | 2022–23** (tonnes) 500 |

Country* Belgium | 2015–16 (tonnes) 0 | 2016–17 (tonnes) 0 | 2017–18 (tonnes) 0 | 2018–19 (tonnes) 0 | 2019–20 (tonnes) 0 | 2020–21 (tonnes) 0 | 2021–22 (tonnes) 0 | 2022–23** (tonnes) 400 |

Country* Indonesia | 2015–16 (tonnes) 2,100 | 2016–17 (tonnes) 2,000 | 2017–18 (tonnes) 6,900 | 2018–19 (tonnes) 13,700 | 2019–20 (tonnes) 2,700 | 2020–21 (tonnes) 2,900 | 2021–22 (tonnes) 3,100 | 2022–23** (tonnes) 500 |

Country* China | 2015–16 (tonnes) 29,600 | 2016–17 (tonnes) 27,100 | 2017–18 (tonnes) 7,700 | 2018–19 (tonnes) 1,600 | 2019–20 (tonnes) 3,500 | 2020–21 (tonnes) 3,300 | 2021–22 (tonnes) 2,000 | 2022–23** (tonnes) 500 |

Country* Korea | 2015–16 (tonnes) 100 | 2016–17 (tonnes) 0 | 2017–18 (tonnes) 0 | 2018–19 (tonnes) 600 | 2019–20 (tonnes) 100 | 2020–21 (tonnes) 200 | 2021–22 (tonnes) 600 | 2022–23** (tonnes) 100 |

Country* All other | 2015–16 (tonnes) 8,000 | 2016–17 (tonnes) 7,300 | 2017–18 (tonnes) 8,500 | 2018–19 (tonnes) 5,300 | 2019–20 (tonnes) 4,100 | 2020–21 (tonnes) 4,900 | 2021–22 (tonnes) 9,000 | 2022–23** (tonnes) 2,100 |

Country* Total | 2015–16 (tonnes) 41,700 | 2016–17 (tonnes) 37,800 | 2017–18 (tonnes) 33,700 | 2018–19 (tonnes) 27,800 | 2019–20 (tonnes) 22,100 | 2020–21 (tonnes) 23,700 | 2021–22 (tonnes) 28,000 | 2022–23** (tonnes) 5,100 |

Source: ABS and IE (Australian Harmonized Export Commodity Classification (AHECC) data by month, classification and destination country, 2022) and Blue Environment.

* Countries ranked by average of last 3 months of exports.

** Partial year across July 2022 to August 2022.

Table 2: Example monthly change in Victorian kerbside recovered plastics, to export country (tonnes per month).

| Country | July 2022 (tonnes) | August 2022 (tonnes) | Change (%) |

|---|---|---|---|

Country Malaysia | July 2022 (tonnes) 600 | August 2022 (tonnes) 500 | Change (%) -17% |

Country USA | July 2022 (tonnes) 300 | August 2022 (tonnes) 200 | Change (%) -33% |

Country Belgium | July 2022 (tonnes) 100 | August 2022 (tonnes) 300 | Change (%) 200% |

Country Indonesia | July 2022 (tonnes) 300 | August 2022 (tonnes) 200 | Change (%) -33% |

Country China | July 2022 (tonnes) 200 | August 2022 (tonnes) 300 | Change (%) 50% |

Country Korea | July 2022 (tonnes) 100 | August 2022 (tonnes) 100 | Change (%) 0% |

Country All other | July 2022 (tonnes) 1,200 | August 2022 (tonnes) 900 | Change (%) -25% |

Country Total | July 2022 (tonnes) 2,800 | August 2022 (tonnes) 2,500 | Change (%) -11% |

Source: ABS and IE (Australian Harmonized Export Commodity Classification (AHECC) data by month, classification and destination country, 2022) and Blue Environment.

Market opportunities

There continues to be significant and growing local demand for high-quality PET, HDPE and PP packaging recyclate for remanufacturing into many applications, if reprocessed to a high level. In addition, excellent export markets exist for high quality sorted/washed flake and pellets, with price premiums available at around 50%–100% the price of virgin resin.

There is significant new rPET, rHDPE and rPP reprocessing capacity in the pipeline, that appears close to covering the local reprocessing shortfall, including scrap plastics caught up in the Australian unprocessed single-polymer plastics export ban that came into force as of 1 July 2022.

However, as much of the new capacity will not be fully operating by July 2022, there will be a capacity shortfall for the reprocessing of higher value bales of single polymer kerbside packaging, such as PET and HDPE bottles, that were previously sent directly to export. This may lead to the need for safe storage or landfilling while local reprocessing capacity catches up with supply from MRFs.

Markets for mixed polymer and lower value post-consumer plastic packaging, such as PET thermoforms, rigid PVC, rigid PS, and mixed polymer scrap bales continue to be underdeveloped or non-existent.

These mixed bales can no longer be exported (as of July 2021), and it is understood that a reasonable proportion of this material is currently being sent to landfill, but this has been trending down over the last 12 months. It is also reported that some of this Victorian material is currently going to South Australia for reprocessing.

Some of the new rPET reprocessing capacity will specifically target PET thermoforms such as strawberry punnets, and with reducing quantities of this format is being laminated with PE or PP, its value as a recovered commodity is increasing. It is anticipated that within 2–3 years the market for thermoformed rPET will be much healthier, and possibly on a par with bottle grade rPET, assuming laminated PET formats continue to be deselected by packaging designers. However, the trend on the adequacy of PET thermoforms reprocessing capacity into the future does require more in-depth analysis.

It Is important to note that rigid PVC and PS based packaging are now being proactively phased out by many, if not all brand owners, and the quantities of these polymers in kerbside collections are already low and continue to fall. Landfill may often be the best fate for rigid plastic packaging made from these polymers, pending their removal from the packaging system.

Continued deselection of PVC and PS, and ongoing improvements in PET, HDPE and PP based packaging design, are anticipated to improve the overall value and recyclability of our PET, HDPE and PP dominated rigid plastic packaging system.

There is significant new capacity that has started operating in the last couple of years, or is reported to be coming online in the next 1–3 years. A summary of this future capacity, that has a kerbside packaging focus, is provided in Table 3.

Note that the estimated capacity figures in this table are provisional. We continue to update this list as information on new reprocessing facility commitments become public. Also note that there are numerous other significant plastics reprocessing projects under development in Victoria (~10–15) that do not relate to kerbside plastic packaging, these are not listed.

It is noteworthy that more than half of the new and planned capacity is being delivered by Pact Group and its partners.

Table 3: Major new or upgraded plastics reprocessing facilities across 2020–2023 (kerbside packaging focussed).

| Facility name | Location | Est. capacity (tonnes per year) | Highest reprocessing level | Other comments |

|---|---|---|---|---|

Facility name Advanced Circular Polymers (ACP) | Location Somerton VIC | Est. capacity (tonnes per year) 20,000–70,000 | Highest reprocessing level Sorting and shredding/granulation | Other comments Non-food grade flake production of PE and PP (mostly). |

Facility name Australian Recycled Plastics | Location Narrabri NSW | Est. capacity (tonnes per year) 5,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments Non-food grade rPET and rHDPE production. |

Facility name Circular Plastics Australia PET – Pact/Asahi/Cleanaway | Location Albury NSW | Est. capacity (tonnes per year) 25,000–30,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments Food grade rPET and rHDPE production. Operating from Dec 2021. |

Facility name Circular Plastics Australia PET – Pact/Asahi/Cleanaway | Location Altona North VIC | Est. capacity (tonnes per year) 20,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments Food grade rPET production. Start-up in 2023. |

Facility name Circular Plastics Australia PET – Pact/Asahi/Cleanaway | Location Laverton VIC | Est. capacity (tonnes per year) 20,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments Food/non-food grade rHDPE and rPP production. Start-up Dec 2022. |

Facility name Pact Group/Astron | Location Wacol QLD | Est. capacity (tonnes per year) 10,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments rHDPE and rPET kerbside reprocessing, also rLDPE film. Start-up TBC. |

Facility name Pact Group/Astron | Location WA | Est. capacity (tonnes per year) 15,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments rHDPE, rPET and rPP kerbside reprocessing. Start-up TBC. |

Facility name Martogg LCM | Location Dandenong VIC | Est. capacity (tonnes per year) 23,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments Food grade rPET production. |

Facility name Martogg LCM | Location VIC | Est. capacity (tonnes per year) >6,000 | Highest reprocessing level Sorting and shredding/granulation | Other comments Food grade rHDPE production. Start-up in July-Sept 2021 period. |

Facility name Recycled Plastics Australia | Location Kilburn SA | Est. capacity (tonnes per year) 20,000–25,000 | Highest reprocessing level Sorting, shredding/ granulation and pelletising | Other comments Non-food grade flake and pellet production PE and PP (mostly). |

Facility name Total | Location - | Est. capacity (tonnes per year) 164,000–224,000 | Highest reprocessing level - | Other comments - |

Note: Updated to June 2022.

Not listed in the table above are the prospective advanced (chemical recycling) projects nationally that are at varying degrees of project development. These will tend not to target the rigid consumer packaging generated by kerbside recycling but will target flexible plastic packaging collected from consumer sources. Projects include:

- APR Plastics, Plastoil Australia and Biofabrik Technologies (~220,000 tonnes per year) – Early-stage project development. Plan to be fully operational in ~5–8 years.

- Brightmark (~200,000 tonnes per year) – Late-stage project development, planned to be operational in 2025.

- Licella and IQ Renew (initially 20,000 tonnes per year) – Late-stage project development, planned to be operational in 2023 or 2024.

- Qenos, Cleanaway and Plastic Energy (~100,000 tonnes per year) – Early-stage project development. Plan to be fully operational by 2025.

- Samsara Eco, CSIRO & Woolworths enzyme recycling (5,000 tonnes per year) – Trial stage in 2022.

Report disclaimer

The information on this report was prepared in conjunction with Blue Environment, IndustryEdge and Sustainable Resource Use (SRU).

While reasonable efforts have been made to ensure that the contents of this publication are factually correct, Recycling Victoria gives no warranty regarding its accuracy, completeness, currency or suitability for any particular purpose and to the extent permitted by law, does not accept any liability for loss or damages incurred as a result of placed upon the content of this publication.

This publication is provided on the basis that all persons accessing it undertake responsibility for assessing the relevance and accuracy of its content.

Recycling Victoria does not accept any liability for loss or damage arising from your use of or reliance on the data. The inclusion of information in this report does not constitute Recycling Victoria’s endorsement of any particular facility, or any associated organisation, product or service.

Accessibility disclaimer

The Victorian Government is committed to providing a website that is accessible to the widest possible audience, regardless of technology or ability.

This page contains two embedded complex image files (Figures 1 and 2) that may not meet our minimum WCAG AA Accessibility standards.

If you are unable to read any of the content of this page, you can contact the content owners for an Accessible version.

Contact email: rvdata@delwp.vic.gov.au

Updated